The Sandwich Generation: Balancing Your Kids' Future With Your Aging Parents' Needs

Anúncios

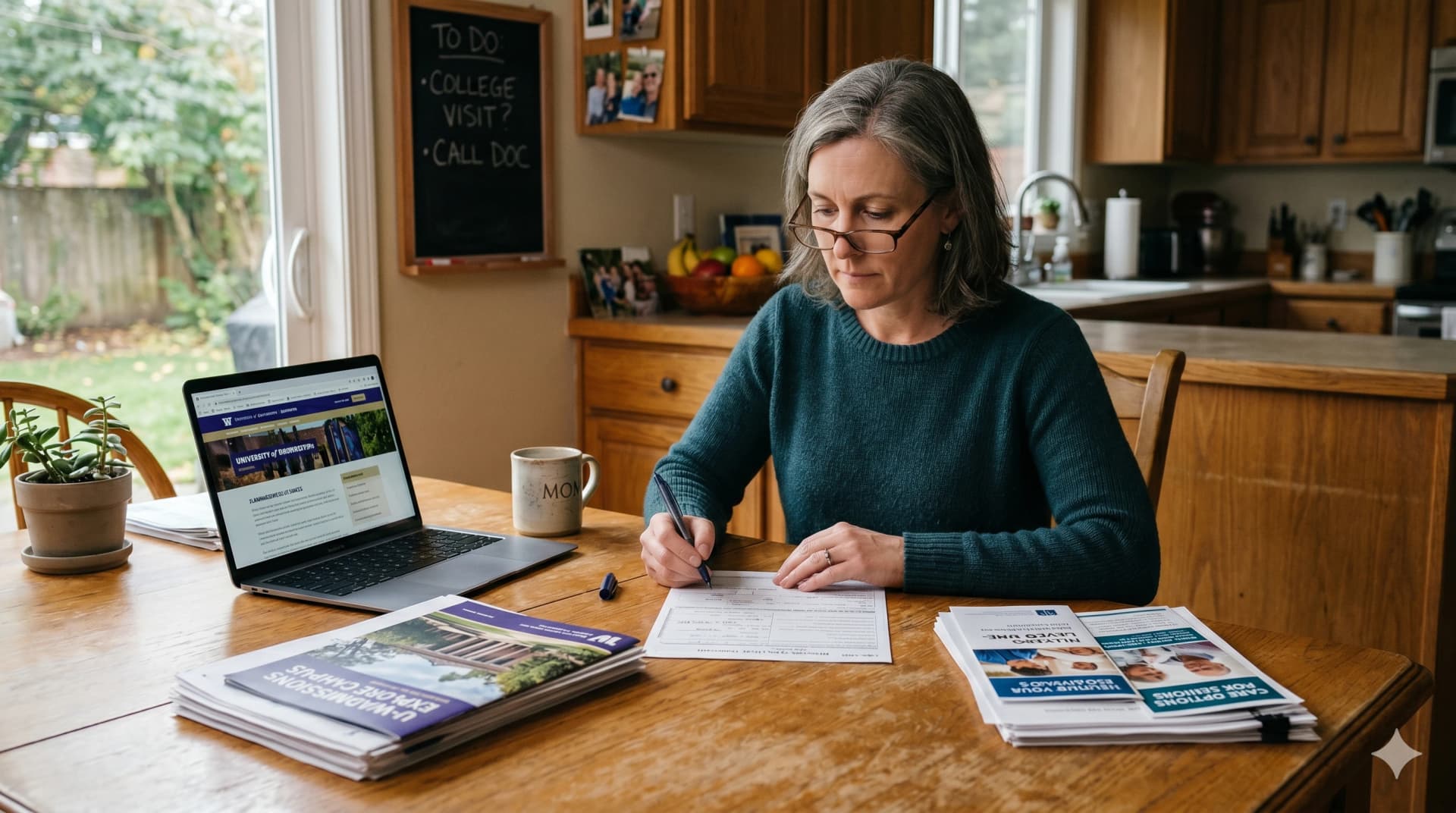

You're helping your teenager research colleges while simultaneously figuring out whether your mom needs in-home care or a memory care facility. Your paycheck has to stretch in two directions at once — and somehow your own retirement savings are also in the picture. If this sounds familiar, you're part of what researchers call the "sandwich generation": adults, typically in their 40s and 50s, who are simultaneously supporting dependent children and aging parents.

According to the Pew Research Center, nearly half of adults in their 40s and 50s are in this position. The financial and emotional weight is real — but with the right framework, it is manageable.

Why the Sandwich Generation Faces a Unique Financial Squeeze

Most personal finance advice assumes a straightforward trajectory: pay off debt, build savings, retire. Sandwich generation households don't have that luxury. Their financial demands arrive from multiple directions at the same time.

On one side, raising children in the US is expensive. Childcare, extracurricular activities, health insurance, and eventually college costs can consume a significant portion of household income. On the other, the cost of eldercare has risen sharply — the median annual cost of a private room in a US nursing home exceeded $100,000 in recent years, and even part-time in-home care carries substantial monthly bills.

Many sandwich generation adults find they are contributing to their parents' expenses while also trying to fund a 529 college savings plan — and their own 401(k) contributions slip as a result. That tradeoff has long-term consequences that are worth taking seriously before they compound.

The Rule Most Financial Advisors Agree On: Fund Your Retirement First

It feels counterintuitive, but the most consistent advice from financial planners for sandwich generation adults is to prioritize their own retirement savings before fully funding a child's college account. The reasoning is straightforward: your children can borrow for college. You cannot borrow for retirement.

That doesn't mean abandoning your kids' futures — it means sequencing priorities thoughtfully. Contribute at least enough to your 401(k) to capture any employer match (that is free money with an immediate 50–100% return), then address other competing demands.

For a deeper look at how small, consistent contributions build wealth over time, our guide on micro-investing and long-term growth explains the mechanics in plain terms.

Having the Conversation With Your Parents Before a Crisis Forces It

One of the most common financial mistakes sandwich generation adults make is waiting for a health emergency to understand their parents' financial situation. By that point, decisions get made under pressure, options are limited, and the costs of reactive planning are high.

A proactive conversation — ideally before any decline in health — covers several key questions:

- Does your parent have a current will, durable power of attorney, and healthcare directive in place?

- What are their sources of income (Social Security, pension, retirement accounts)?

- Do they have long-term care insurance, and if so, what does it cover?

- What are their preferences for care — in-home support, an assisted living community, or moving in with family?

Our guide on how to talk to aging parents about their finances and legacy plans walks through how to approach this conversation without it feeling confrontational.

Strategies That Actually Help When You're Being Pulled in Both Directions

There is no magic formula, but several practical moves tend to reduce the financial strain for sandwich generation households:

Build (and protect) your emergency fund

Caregiving situations generate unpredictable expenses. A hospital stay, a home modification for mobility, or a gap between care arrangements can arrive without warning. A liquid emergency fund of three to six months of essential expenses is your buffer against having to raid retirement accounts or take on high-interest debt. If you are starting from zero, our guide to saving your first $1,000 stress-free lays out a simple starting framework.

Explore federal and state eldercare resources

Medicare, Medicaid, and the Administration for Community Living offer programs that many families don't realize their parents qualify for. The Eldercare Locator (a public service of the US Administration on Aging) can connect you with local services — from meal delivery to transportation to in-home assistance. Using available public resources reduces how much comes out of your own pocket.

Consider the tax benefits available to caregivers

If you are providing more than half of a parent's financial support, they may qualify as your dependent for IRS purposes, potentially allowing you to claim the Credit for Other Dependents. Dependent care FSAs at some employers can also cover certain adult dependent care expenses. Review IRS Publication 503 or consult a tax professional to understand what you may qualify for.

Have an honest conversation with your siblings

Financial responsibility for aging parents is not always distributed equally. If one sibling lives nearby and provides most of the hands-on care, that person's financial contributions (time off work, transportation costs, household accommodations) should be part of the family discussion. Documenting an explicit cost-sharing or time-sharing agreement with siblings reduces resentment and prevents one person from absorbing a disproportionate financial burden.

Your Next Steps

Anúncios

The sandwich generation squeeze is real, but the worst outcome is paralysis — continuing to absorb competing demands without a deliberate plan until something breaks. A few concrete actions can shift the dynamic:

- Schedule a 30-minute financial check-in with your parents within the next month. You don't need to cover everything at once — just establish the conversation.

- Log into your 401(k) portal and confirm your contribution rate captures any available employer match.

- Use the CFPB's free consumer tools to audit your household budget and identify where resources are actually going.

- If you haven't already, consult a fee-only financial planner (search NAPFA.org for advisors who work without commissions) who has experience with multigenerational financial planning.

Being sandwiched doesn't mean you have to absorb all the pressure alone. Acknowledging the situation, mapping the resources available to you, and making deliberate choices — even imperfect ones — puts you in a fundamentally better position than reacting to each crisis as it arrives.

Anúncios